Starlink out front, but can it stay there?

Satellite direct-to-device market could be worth tens of billions once rolled out

The SpaceX launch on Oct. 5 added 22 satellites to its constellation of nearly 4,300 last week, putting the company closer to the 12,000 it has planned — and with regulatory paperwork filed for 30,000 more, traditional operators have a formidable rising power to account for.

Starlink’s constellation constitutes 4,268 operational units at the time of writing, according to satellitemap.space, a browser-based satellite tracking database.

“In the past three years between 64% and 79% of all satellites launched into space from Earth did so on a SpaceX rocket,” said Claude Rousseau, research director at Northern Sky Research (NSR) at a recent presentation. “Of that number, a good proportion were Starlink satellites.”

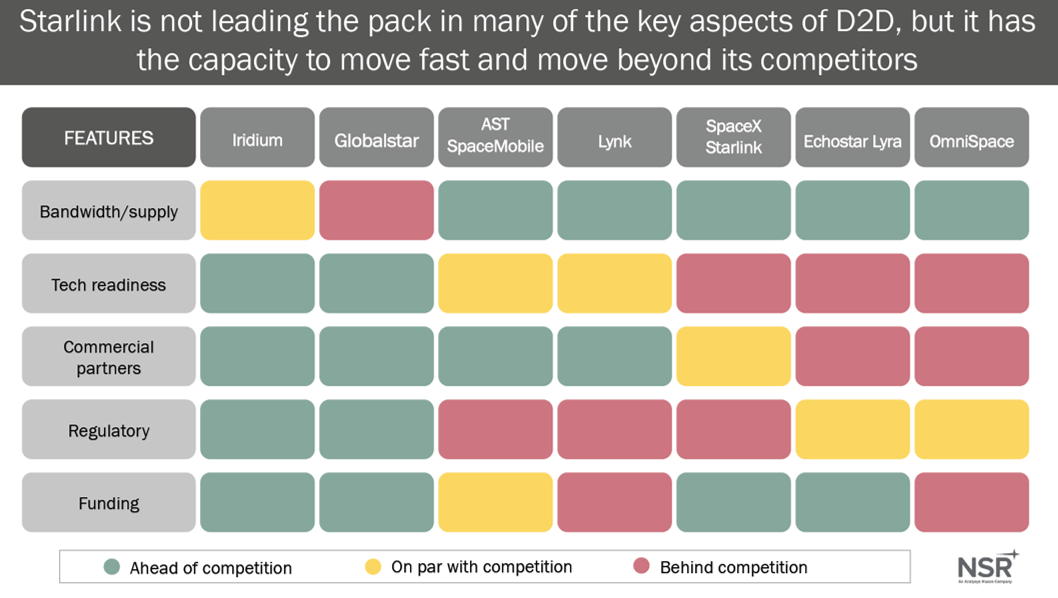

But some industry experts say consolidation and synergies will enable other providers, including Amazon’s Project Kuiper, to compete with Starlink.

“We believe consolidation and synergies will enable geosynchronous providers and others in non-geosynchronous space to compete with Starlink — and eventually Kuiper, which we also believe is going to be formidable, potentially an even bigger market threat,” said Jose Del Rosario, research director at NSR.

The growth of Starlink

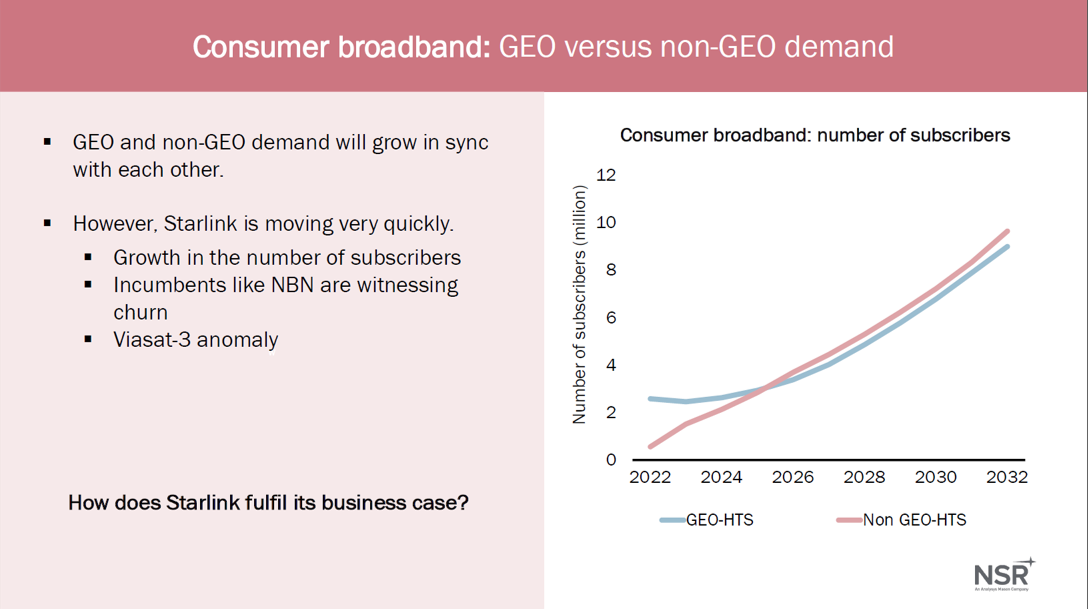

Despite only joining the broadband market in early 2021, Starlink’s rise has been unprecedented, rocketing to 2 million subscribers in September, up from 1.5 million in May, and 1 million at the close of 2022, according to data from its operator, SpaceX.

“When we compare their activity to two bigger players, say, Hughes and Viasat, Starlink has grown fast,” said Lluc Palerm, principal analyst at NSR in his section of the presentation. “Hughes is at about 1.5 million subscribers and Viasat is at 0.7 million after years in the industry.”

Palerm also mentioned the in-orbit troubles suffered by Viasat this year as yet another avenue by which Starlink has consumed market share. However, he insisted geosynchronous offerings still serve a large addressable market, allowing for a strong effort against Starlink.

“We don’t expect geosynchronous broadband to sit idly by and Starlink walk all over them,” NSR’s Del Rosario added. “Geosynchronous players have inherent advantages like a large installed base enabling competitive pricing, high bandwidth and market access. Starlink has covered 50-plus countries in three years, but over decades, the geosynchronous players already span over 70. We think they can scale competitively with Starlink with the right strategy.”

Del Rosario insisted it wasn’t all rosy for Starlink, highlighting various commercial hiccups including only recently resolved regulatory hurdles in Indian markets, and the company’s recently resolved policy of subsidizing the prices of their flat-panel antennas.

Flat panel antennas, though highly sought in the connectivity market for their technical capability have not been able to reach the price points their consumers need to form stable markets. With no short-term solutions, and a supply chain crisis, a subsidized price can be a costly, yet foolproof way of ensuring competitivity.

“Their flat panel antennas currently sit at a $600 price point, which remains very high,” Del Rosario said.

Palerm pointed to Starlink’s fascination with vertical integration as a weakness in the market.

“Starlink is not very good at working with the rest of the connectivity ecosystem,” he said, adding that the company is “usually very closed and centered on working with their own technology. They need to be aligned with chipset and smartphone manufacturers as well as mobile operators.”

In fact, NSR analysts predict these caveats could inform Kuiper’s path to market, allowing it to sidestep the early mistakes of Starlink by learning from them.

Two prototype Kuiper satellites were carried into low-Earth orbit Oct. 6, followed by successful first contact.

Market potential in satellite-to-device

The potential of the satellite connectivity market is vast, with the power to influence many existing markets through broadband, IoT and mobility services.

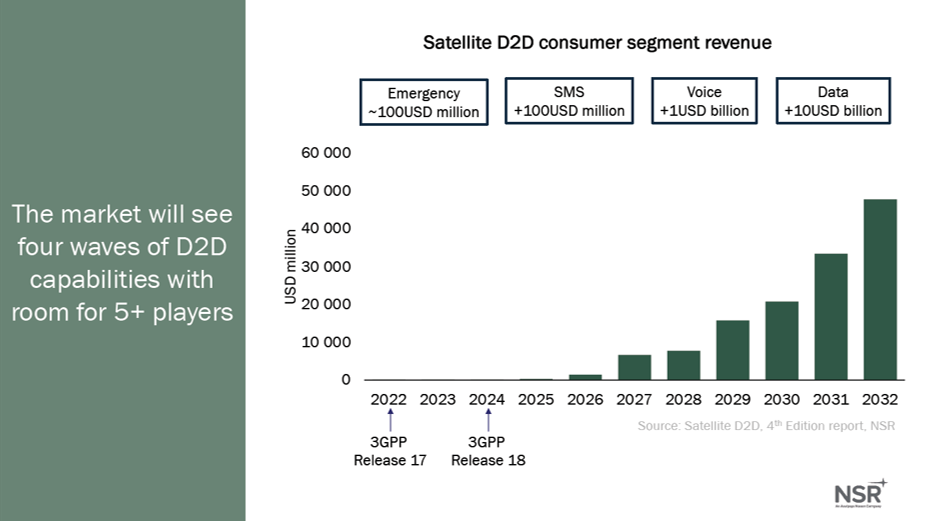

Palerm introduced the four stages NSR has identified for the satellite direct-to-device service market:

- Emergency coverage, which NSR values at $100 million per year;

- Narrowband messaging, to be worth about $500 million per year.

- Voice, at $1 billion per year; and

- Data services, which NSR values at tens of billions of dollars per year.

With bitter competition between players, there’s no guarantee that SpaceX will come out ahead due to scale alone. Their competitors are ahead of them when it comes to the technical needs of enterprise and government, as well as associated regulatory efforts, Palerm said.

“Across a number of business model analyses, including optimistic, balanced, and conservative scenarios, we concluded that Starlink is going to be profitable in the short term with a lot of growth moving forward. But there’s still plenty of moves left to make,” he said.