Valuations and deal activity in the 2021 space economy sit at unprecedented levels, and are expected to remain high with the onset of special purpose acquisition companies (SPACs).

There were 32 space mergers and acquisitions in the first nine months of the year — more than the 29 deals in all of 2020 — according to investment bank KippsDeSanto & Co.’s Fall 2021 MarketView report on aerospace/defense and government technology services.

The bank has completed eight space-related deals in the last 24 months, Managing Director Karl Schmidt noted.

KippsDeSanto in August advised middle market private equity firm J.F. Lehman & Company on the sale of component maker BEI Precision Systems & Space for an undisclosed sum, Schmidt noted, adding that J.F. Lehman had previously acquired BEI Precision Systems & Space in 2017 for an undisclosed sum, in a transaction in which it was also advised by KippsDeSanto.

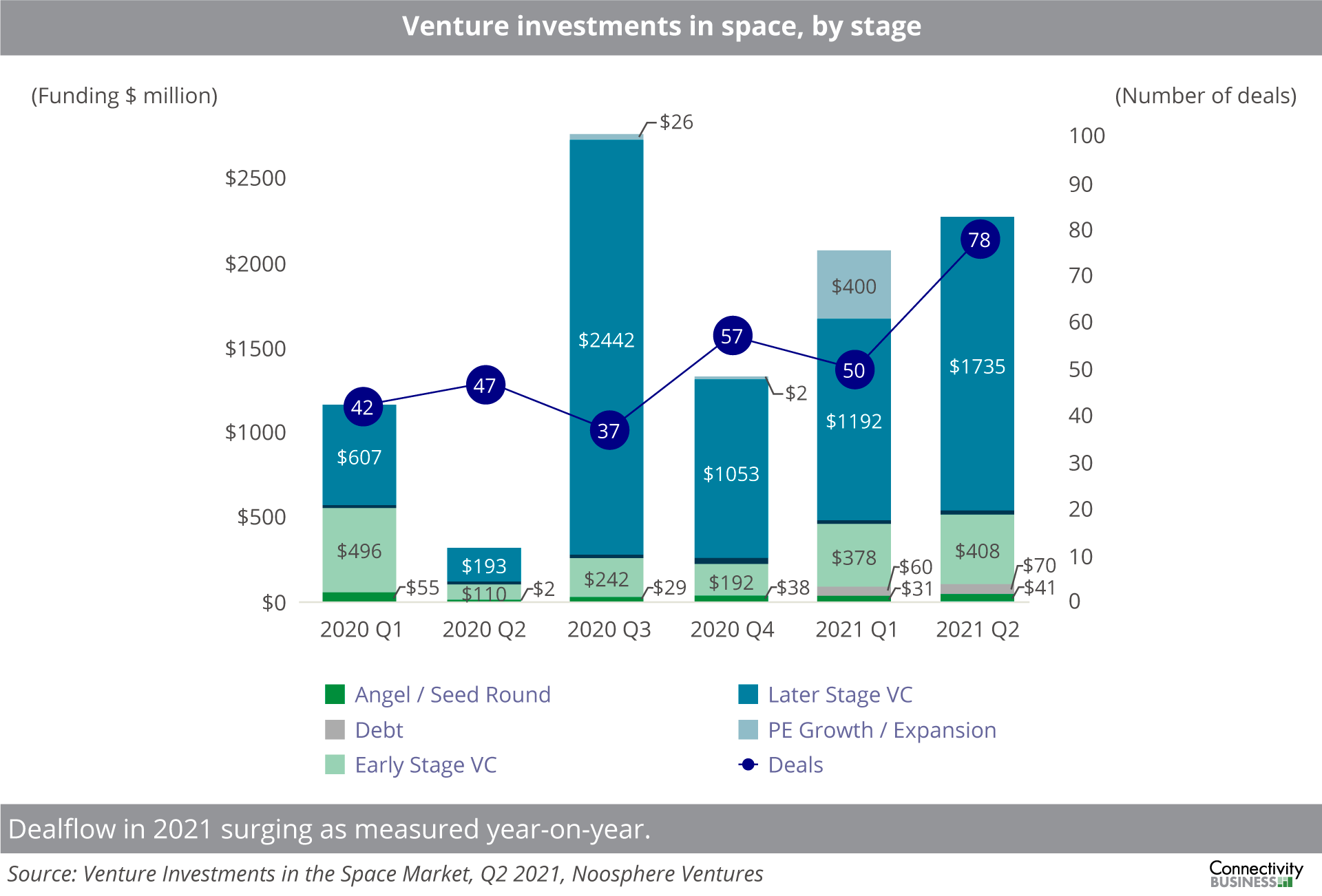

A Q2 2021 report by investment firm Noosphere Ventures, “Venture Investments in the Space Market,” echoes the remarkable investment in the space industry, stating that venture investment in the quarter totaled $2.2 billion, including the add-on of a SpaceX round that raised $1.2 billion.

Satellite is experiencing “a long-duration market with a Fed that never runs out of ink,” Promus Ventures founder and Managing Partner Mike Collett said during a panel discussion about return on investment (ROI) at the Satellite Innovation 2021 conference earlier this month.

Panelists described a diversity of approaches to space investment. Starbridge Venture Capital seeks to invest in offerings that can play a role in terrestrial networks as well as space connectivity, said Steven Jorgenson, founder and general partner. Companies that can play a role in the larger terrestrial ecosystem will be faster to profitability and faster to exit than those whose business only plays a role in space, he added.

Goldman Sachs is examining innovations made possible by developments that are driving costs down for everyone, such as cheaper launch services, said Shireen Sharma, vice president of the technology, media and telecom group. As companies plan to “do things in space that they’ve never done before,” Goldman Sachs is looking for the right innovative companies “not just for the next couple of years, but really the next 10 to 20 years as well,” Sharma added.

Return on Investment

Space-related investors are willing to pay higher multiples, KippsDeSanto’s Schmidt said. “We’re seeing deals at 2x EBITDA higher [than in the past and] it’s pushing into our middle market M&A.”

The type of product determines the range of the multiple, Schmidt added, noting that software sells for more, as does equipment that can transform the market, such as Raytheon’s (NYSE:RTX) September acquisition of privately held space electronics manufacturer SEAKR Engineering.

Companies, especially government contractors, understand the need to have a space capability and are eager to make an acquisition “even if it’s not the best company they can buy,” Schmidt said. “I would say half of recent buyers were not in space but wanted a space asset” because they see a rapidly growing market.

Just as different types of companies deliver different returns, different investors also require different ROIs. Starbridge seeks an ROI of 33% per year over a 10-year period, Jorgenson said. Companies that don’t have high growth rates such as those in commodity component businesses are harder to invest in compared to “something that’s actually moving the industry or providing 30% plus efficiencies,” he noted.

Meanwhile, Promus Ventures has a long-term view, according to Collett. “We always say that if you grow big enough and strong enough, capital will come and exits will come,” he said. “We like our investors, our founders to want to hold on to these shares.”

Investors want to know whether a company will dominate its sector or be overshadowed by its competitors, according to Goldman Sachs’ Sharma. As companies seek to capture the customer, “you are going to see a lot of horizontal M&A,” she added.

In contrast, where the technology is developing rapidly and the future is unclear, a lower valuation is reasonable, she added.

The closer a company is to reducing the technological risk, the closer it is to a full ecosystem, Sharma said. Investors are more likely to invest if they are convinced that it is one of three or four winners in its segment “and the more they can believe our projections,” she said.