SPAC funding accumulates amid mixed outlook for financing trend in commercial space

SPACs possess $131B in capital

While special purpose acquisition companies (SPACs) possess $131 billion in dry powder, the outlook for the financing trend in commercial space appears mixed.

Investor enthusiasm for SPACs is taking a hit for several reasons, including climbing redemption rates. This dynamic is important as SPAC shareholders have the option to redeem their shares when a merger with an operating company closes, rather than keep them in the merged company. Higher redemptions mean less capital to deploy.

However, recent regulatory activity in Asia and Europe is paving the way for increasing SPAC deals, even as the trend cools in the U.S., which was the pathfinder for the trend in 2020.

SPACs do keep generating enthusiasm in commercial space. On Sept. 9, Earth observation company BlackSky (NYSE:BKSY) completed its SPAC transaction with Osprey Technology Acquisition. The combined company received $283 million in proceeds, comprised of $103 million in cash held in trust by Osprey and the remainder in public investment in private equity.

The deal had a spillover benefit, as artificial intelligence company Palantir Technologies (NYSE:PLTR) recently made an undisclosed investment in BlackSky and entered into a multiyear software subscription agreement with the company.

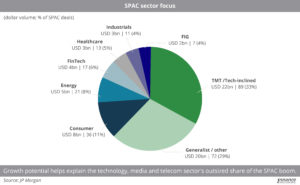

SPACs by the numbers

Some 423 SPACs are searching for merger partners to deploy their capital, JP Morgan noted in its recent weekly analysis. And in September alone, 31 SPAC IPOs were announced, raising billions in financing.

There are currently 122 SPAC mergers announced and pending close, representing $38 billion in proceeds and $29 billion in committed PIPE proceeds.

And the SPAC IPO pipeline remains robust, with some 280 SPACs publicly on file seeking to raise $66 billion, JP Morgan said. Of these, 36% of these firms are repeat issuers.

However, the median redemption rate for North American SPAC deals completed in July was almost 50%, according to Spacresearch.com. If the trend continues, it could undermine the notion that SPACs are a more predictable way of going public than a traditional IPO.

Cubesate operator Spire (NYSE:SPIR), which operates a constellation that provides weather and tracking data, stomached a redemption rate of about 90% when it closed its deal with SPAC NavSight Holdings (NYSE:NSH) on Aug. 16, receiving $245 million of private investment in public equity and $20 million in cash in trust. Spire used the financing Sept. 14, announcing the acquisition of automatic identification system provider exactEarth (TSX:XCT) for $161.2 million.

In-space transportation company Momentus (NASDAQ:MNTS), which closed its SPAC merger Aug. 12 with Stable Road Acquisition Corp. (NASDAQ:SRACU), had a redemption rate of 20%.

SPAC enhancement?

SPACs got a boost in early September, when the Singapore Exchange announced that it is preparing to roll out easier guidelines for listings of these transactions in the Asian nation, which would make it the first major exchange in that region to accept such investment vehicles.

The Singapore Exchange’s regulatory arm is considering easing a minimum of $223.2 million market value proposal for SPACs and a proposal that warrants cannot be detached from underlying shares. SGX faces prospects of losing out in courting Southeast Asian start-ups looking to list in their home markets or in the U.S. In other markets in the region, Hong Kong and Indonesia are taking tentative steps for the potential listing of SPACs.

SPAC deals also got a recent life in the U.K. as the Financial Conduct Authority regulatory authority announced in August that they will only have to raise a minimum of about $137 million at IPO, down from a planned $273 million. SPACs were set to see a potential flow of capital from Europe as the trend took off in the spring while the torrid space of these transactions cooled in the U.S.